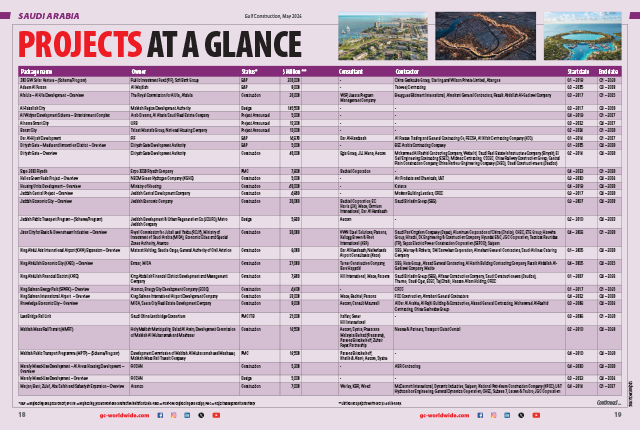

Saudi Arabia’s construction sector has entered its next phase of growth under a far sharper strategic lens, following a landmark announcement from the kingdom’s sovereign wealth fund Public Investment Fund (PIF) that is set to redefine how projects are prioritised, funded and delivered across the kingdom.

The approval of PIF’s 2026–2030 strategy by its board, chaired by His Royal Highness Prince Mohammed bin Salman bin Abdulaziz Al Saud, Crown Prince and Prime Minister, signals a decisive shift away from a purely expansion-driven model towards one anchored in integrated economic ecosystems, capital discipline and long-term value creation.

At the core of this strategy is a restructuring of PIF’s vast portfolio of 13 strategic sectors into six interconnected economic ecosystems, designed to strengthen linkages between industries and unlock broader opportunities for private-sector participation. As PIF Governor Yasir Al-Rumayyan emphasised, the approach builds on the fund’s central role in driving economic diversification under Saudi Vision 2030, while sharpening financial returns and reinforcing the kingdom’s long-term prosperity.

For the construction industry, which sits at the intersection of nearly all these sectors, the implications are profound: project delivery is no longer just about scale, but about integration, sequencing and measurable economic impact.

Another key trend that is emerging from lessons learned under the current geopolitical situation by the Gulf region is a focus on creating a geo-economic corridor linking the Arabian Gulf to the Mediterranean, which will reposition Saudi Arabia at the centre of regional and intercontinental trade. In line with this, the kingdom has awarded Spain’s Typsa the lead design consultancy contract for its long-delayed Landbridge railway, marking fresh momentum for the $27-billion project aimed at linking the Red Sea and Gulf coasts, according to industry reports. Saudi Arabia is also reported to be pushing for the joint studies for a railway link project connecting Saudi Arabia and Turkey via Jordan and Syria to be completed before the end of the year.

In the current Gulf geopolitical climate, NEOM Port is positioning itself as a strategically important alternative gateway within Saudi Arabia’s Vision 2030 framework. As global shipping increasingly seeks to diversify away from chokepoints, NEOM Port is being developed as part of an emerging Europe-Middle East trade corridor that links Mediterranean routes through Egypt to the Red Sea and then overland into the Gulf.

After years of announcing ever-more ambitious giga-projects, the kingdom is now applying a filter of fiscal discipline. Vision 2030’s $1.7 trillion pipeline remains intact in aspiration, but execution is being sequenced around fixed event deadlines – World Expo 2030 (October 2030-March 2031) and the FIFA World Cup 2034 – and those projects demonstrating near-term economic returns, particularly in tourism, logistics and renewable energy.

The suspension of The Line at NEOM, the recalibration of Trojena and the Mukaab, and the cancellation of multiple NEOM sub-contracts in late 2025 and early 2026 have been widely reported. Yet these setbacks must be set against a broader picture where Diriyah, Qiddiya, the Red Sea, King Salman Park, King Salman International Airport and Expo 2030 site preparation are all accelerating.

Jeddah Tower ... 100-storey milestone.

The total value of giga-project contract awards reached $196 billion by end-2025, up 20 per cent from the previous year, according to Knight Frank. Of 17 giga- and mega projects along the western coast alone, $57 billion in contracts have been awarded, with a further $187.2 billion in the pipeline.

Against this backdrop of large-scale ambition and strategic repositioning, cost pressures in Saudi Arabia, and in particular the capital, are becoming increasingly pronounced. Riyadh has now emerged as one of the most expensive construction markets in the MENA region, with average costs reaching $3,112 per sq m, according to Turner & Townsend’s KSA Market Intelligence 2025 report. Yet rather than dampening activity, these elevated costs underscore the intensity of development and sustained confidence, particularly across tourism, logistics, digital infrastructure and residential sectors.

Riyadh is at the heart of the kingdom’s transformation and is leading Saudi Arabia’s giga-project agenda, with landmark developments such as Diriyah, Qiddiya, Misk City, King Abdullah Gardens, King Salman Park and Sports Boulevard redefining the city’s urban fabric.

Projects worth over $237 billion have been announced across real estate, infrastructure and transportation sectors since 2016, with $44 billion already awarded in construction contracts, according to Faisal Durrani, Partner and Head of Research MENA, Knight Frank.

These investments will support the projected city population boom from seven million in 2022 to 10.1 million by 2030 with over 340,000 homes, 4.8 million sq m of offices, 3 million sq m of retail and close to 30,000 new hotel rooms.

In addition, Western Saudi Arabia is emerging as a centrepiece of Vision 2030, said Knight Frank, with giga projects such as NEOM and The Red Sea Project redefining the region through futuristic development, protected natural landscapes and luxury tourism destinations.

STRATEGIC RECALIBRATION

PIF’s 2026–2030 strategy introduces three distinct investment portfolios. The Vision Portfolio will focus on deepening integration across priority sectors and maximising the value of PIF-backed developments within six ecosystems, creating a more cohesive pipeline of projects and enhancing opportunities for contractors, suppliers and investors. The Strategic Portfolio will concentrate on optimising returns from key assets while supporting the global expansion of Saudi companies, and the Financial Portfolio will target sustainable returns through diversified global investments, strengthening PIF’s balance sheet and its ability to fund future development cycles.

Within this framework, construction activity is directly shaped by the ambitions of the six major ecosystems. The Tourism, Travel and Entertainment ecosystem alone will drive the creation of more than 100,000 hotel rooms, over 70 new tourism experiences and critical infrastructure for global events including 2034 FIFA World Cup and Expo 2030 Riyadh. Flagship developments such as NEOM, Qiddiya and The Red Sea Project remain central to this push, alongside major aviation infrastructure including King Salman International Airport.

Equally significant is the Urban Development and Livability ecosystem, which targets homeownership rates of 70 per cent through the delivery of up to 190,000 housing units by 2030 and millions of square metres of commercial space. Developments led by ROSHN Group and New Murabba are expected to anchor this expansion, reinforcing construction demand across residential, mixed-use and urban infrastructure segments.

Industrial growth will also feed directly into construction pipelines. The Advanced Manufacturing and Innovation ecosystem aims to build export-oriented sectors spanning artificial intelligence, automotive and pharmaceuticals, supported by industrial clusters and logistics infrastructure.

A number of landmark developments are taking shape in Qiddiya City including the Prince Mohammed bin Salman Stadium.

Meanwhile, the Industrials and Logistics ecosystem will expand mining, ports and supply chains, with key players such as Ma’aden and Bahri driving demand for heavy industrial facilities, transport corridors and logistics hubs.

In parallel, the Clean Energy, Water and Renewables Infrastructure ecosystem is set to accelerate the development of large-scale renewable projects, targeting up to 100 GW of capacity. This alone represents one of the largest construction opportunities globally, spanning solar and wind farms, transmission networks and water infrastructure, led by entities including ACWA Power.

These ambitions are underpinned by the scale of PIF’s recent investment activity. Between 2021 and 2025, the fund deployed approximately SAR750 billion ($200 billion) into domestic projects, accounting for around 70 per cent of its total investments, while maintaining average annual returns above seven per cent since 2017.

Al-Rumayyan underscored that this evolution builds upon the PIF’s pivotal role in leading economic diversification, leveraging the kingdom’s advanced infrastructure and globally connected liquidity to safeguard national wealth for future generations.

As the construction industry navigates a complex phase of strategic recalibration, the PIF’s refined focus provides a clear hierarchy of priorities, moving away from sheer volume toward long-term viability and high-impact economic synergy.

This recalibration comes at a time when Saudi Arabia remains the world’s busiest construction market, even as it balances fiscal realities with the drive to transform the economy. While the total pipeline remains unparalleled, developers and state-backed entities are now emphasising sequencing, efficiency, and return on investment.

According to the General Authority for Statistics (GASTAT), Saudi Arabia’s construction sector accounted for about eight per cent of economic output in 2025, equivalent to roughly SAR383 billion, underscoring its role as one of the kingdom’s largest non-oil contributors alongside trade and manufacturing. The sector is increasingly influenced by fixed international commitments. The countdown to Expo 2030 Riyadh and the FIFA World Cup 2034 has introduced non-negotiable deadlines that are accelerating decision-making in transport, hospitality, and urban infrastructure.

INFRASTRUCTURE & TRANSPORT

Infrastructure remains the single largest construction sub-sector, accounting for 36.6 per cent of total market value in 2025, according to research firm Mordor Intelligence. The Saudi 2026 national budget allocates SAR35 billion to infrastructure and transportation, reflecting the government’s sustained capital commitment. Meanwhile, Saudi Electricity Company (SEC) has earmarked $126 billion until 2030 for expanding and modernising transmission and distribution grids to accommodate growing electricity needs and renewable integration.

Metro & Rail: The Riyadh Metro – the world’s longest driverless metro network at 176 km across six lines – continues to expand. A Webuild-led consortium (with L&T, Nesma and Alstom) has been awarded a contract for an 8.4-km Red Line extension incorporating five new stations, three underground, with a TBM-bored tunnel section. The extension will connect the existing network to Diriyah, a UNESCO World Heritage Site.

Plans are now on the anvil for the proposed seventh line of the metro: The Royal Commission for Riyadh City (RCRC) has received commercial proposals for the design and build contract of Line 7, which will be about 65 km long and have 19 stations, linking landmark destinations such as Qiddiya Entertainment City development, King Abdullah Gardens, King Salman Park, Misk City and Diriyah Gate.

Meanwhile, plans for the Jeddah metro also appear to be revived with the Jeddah Development Authority reported to have issued preliminary design consultancy tenders for the Blue Line, a 35-km network linking King Abdulaziz International Airport to the Haramain High-Speed Railway station.

Beyond urban transit, nationally significant freight infrastructure is advancing through the Saudi Railway Company’s $7-billion Saudi Landbridge project, which is planned to be completed in phases by 2034. TYPSA has just secured a contract, issued by Saudi Arabia Railways after a 2025 tender for the network spanning more than 1,500 km. This freight-led network will strengthen east-west connectivity linking Jeddah with Riyadh and onward connections to the North-South Railway and Dammam. (see Saudi Focus, Page 99).

Meanwhile, plans have also been announced for the Qiddiya High-Speed Rail Project. The Royal Commission for Riyadh City (RCRC), in partnership with the National Center for Privatization & PPP and Qiddiya Investment Company, has requested expressions of interest (EOIs) for the project, which will be implemented under a public-private partnership (PPP) model. The line aims to connect King Salman International Airport, King Abdullah Financial District (KAFD), and Qiddiya City in just 30 minutes, via a high-speed rail line of 250 km/h.

Also on the cards is the proposed Riyadh-Doha railway, the region’s first high-speed rail link between two neighbouring countries. The 785-km network will serve Riyadh, Hofuf, Dammam, and Doha, with five stations in total.

Airports: King Salman International Airport – the $30-billion redevelopment of the existing King Khalid International Airport site – represents one of Riyadh’s most significant infrastructure developments, with construction activity now under way following the January commencement of works on a 4,200-m third runway. Being delivered by FCC Construcción in partnership with Al-Mabani General Contractors, the runway will increase hourly aircraft movements from 65 to 85 while enhancing operational resilience.

Three international contractor consortia have now been shortlisted for early contractor involvement (ECI) work on Terminal 6, which will add 40 million passengers per year of capacity ahead of Expo 2030 Riyadh.

The airport authority has also signed seven MoUs with leading Saudi real estate companies to develop mixed-use projects across its 12-sq-km real estate footprint, within an overall 57-sq-km masterplan. When fully operational, the airport will serve 100 million passengers annually and handle over two million tonnes of cargo.

The Red Sea International Airport ... under development.

Beyond the capital, the government is prioritising airports that serve specific economic and tourism giga-projects. The Red Sea International Airport, which began operations for domestic flights in late 2023, is continuing its phased expansion to reach a capacity of one million guests annually by 2030. It is distinguished by its sustainability focus, being the first in the kingdom to supply Sustainable Aviation Fuel (SAF) and operating entirely on renewable energy.

In the Asir region, the Abha International Airport is undergoing a significant transformation. As of early 2026, the project is nearing a contract award for a public-private partnership that will expand the terminal area from 10,500 to 65,000 sq m. This upgrade is designed to boost capacity from 1.5 million to 13 million passengers, positioning Abha as a major cultural tourism destination.

Other airport projects that will be developed under the PPP model include those planned for Taif and redevelopment of Prince Naif Bin Abdulaziz International Airport in Qassim, which are currently in the bidding stage.

The new Taif International Airport will be located 21 km southeast of the existing Taif airport, and on completion will boast a capacity of 2.5 million passengers by 2030.

Plans for a new world-class airport in Makkah have moved forward with the Royal Commission for Makkah City and Holy Sites having approved strategic and investment plans for this facility, which is intended to serve pilgrims and residents without compromising the economic viability of nearby hubs in Jeddah and Taif (see Saudi Focus, Page 100).

Another key project is the expansion of the Hajj Terminal expansion at Jeddah’s King Abdulaziz International Airport, for which PACE and SOM have recently been appointed as lead design consultants.

Ports & Logistics: Saudi Arabia’s ports authority (Mawani) continues to expand logistics capacity, having signed a SAR250 million lease agreement with Sultan Logistics for a 200,000-sq-m logistics park at Jeddah Islamic Port. Mawani’s broader strategy, under the National Transport and Logistics Strategy, targets logistics parks within and beyond the kingdom’s major ports. A similar SAR200-million park will come up at Dammam’s King Abdulaziz Port.

Meanwhile, SAL Saudi Logistics Services Company and Sela Company have signed a SAR4 billion agreement to develop a state-of-the-art logistics zone within Falcons City, King Khalid International Airport in Riyadh and national transport corridors.

Roads: The Royal Commission for Riyadh City is pressing ahead with a comprehensive SAR29-billion programme to upgrade and expand the capital’s arterial road network, aimed at easing congestion, improving connectivity, and supporting the city’s long-term urban growth.

At the core of this effort is the Riyadh Main and Ring Road Axes Development Programme, which will add more than 500 km of new and upgraded roads. The multi-phase programme aims to increase overall road capacity by up to 85 per cent, significantly enhancing mobility and reinforcing Riyadh’s position as a leading infrastructure hub.

The programme is being delivered through a phased, package-based approach, with each stage targeting key corridors to ensure balanced network development across the city. The latest phase, Package Three, was awarded in late 2025 at a value exceeding SAR8 billion. It covers the construction of 61 km of roads, 32 bridges and six tunnels, focusing on critical northern and western corridors, with completion scheduled within four years.

Earlier phases of the programme are already under way. Package One, launched in August 2024 with a budget of SAR13 billion, includes major works such as the 56-km Second Southern Ring Road, additional bridges parallel to Wadi Laban Bridge, and key sections of Thumamah Road and associated corridors.

Package Two, launched in February 2025 with a value exceeding SAR8 billion, comprises eight projects aimed at improving internal traffic flow and strengthening links between residential and commercial districts.

Meanwhile, Saudi Arabia’s Roads General Authority (RGA) and the National Centre for Privatisation are progressing the One-Stop Station (OSS) project, a DBFOM PPP (design, build, finance, operate, maintain public–private partnership) that will transform the kingdom’s 73,600-km intercity road network with modern fuel, hospitality and rest facilities. Multiple consortia have been shortlisted.

STADIUMS

Saudi Arabia is accelerating delivery of major stadium projects as part of its broader strategy to enhance sports infrastructure ahead of global events, including the AFC Asian Cup 2027 and the FIFA World Cup 2034.

In Riyadh, the Ministry of Sports has invited prequalification bids for the preliminary works the King Salman Stadium, the largest-capacity stadiums in Saudi Arabia with a capacity exceeding 92,000 seats.

Aramco Stadium in Al Khobar ... well advanced.

Designed by US-based Populous, the stadium integrates elements inspired by Saudi Arabia’s natural landscape and cultural heritage, and is located adjacent to King Abdulaziz Park (see Saudi Focus, Page 97).

In the Eastern Province, construction of the Aramco Stadium in Al Khobar is well advanced. The 45,000-seat venue is being developed in collaboration with the BESIX–Albawani joint venture. The stadium, also designed by Populous, is being delivered under a fast-track programme to support Saudi Arabia’s football hosting ambitions.

Meanwhile, the Prince Faisal bin Fahad Sports City in Riyadh is being developed under a public-private partnership model. Led by the Ministry of Sports in collaboration with the National Centre for Privatization and PPP and Riyadh Municipality, the project has entered the EoI and RFQ stages. Structured as a design, build, finance, operate and maintain (DBFOM) contract over 20–30 years, the scheme includes a new 47,000-seat stadium in Al Malaz.

POWER & WATER

Saudi Arabia continues to advance its clean energy transition, with significant milestones achieved across utility-scale power and water infrastructure. Energy infrastructure is one of the most active and capital-intensive construction sub-sectors.

The renewable energy sector saw a landmark achievement in March 2026 with the completion of the 348.6 MW El Saad Solar Plant. Developed by a consortium including Al Ghazala Energy Company and Jinko Power, the facility, located 85 km east of Riyadh, was delivered by EPC contractor Elsewedy Electric.

Earlier, in December 2025, Acwa Power reached financial close on seven giga-scale renewable energy projects totalling 15 GW. These projects, including five solar and two wind facilities, are being developed under the National Renewable Energy Program (NREP) in partnership with Badeel and the Saudi Aramco Power Company, with commercial operations targeted between late 2027 and mid-2028.

In the conventional power sector, Saudi Electricity Company s driving major capacity expansions, most notably the $1.4 billion Rabigh 1 Expansion Project. The 1,200 MW combined-cycle gas turbine (CCGT) plant, being delivered by a consortium of Elsewedy Electric and Siemens Energy, is designed to be carbon-capture ready and is expected to serve 500,000 residential units annually. Additionally, Acwa Power achieved financial close for the $2.9 billion Qurayyah CCGT expansion, a 3,010 MW facility in the Eastern Province.

The kingdom is also reinforcing its utility resilience through strategic water and storage investments. Last November, the SAR8.5 billion Jubail–Buraydah Independent Water Transmission Pipeline achieved financial close. Stretching 587 km, the project will transport 650,000 cu m of desalinated water per day, serving over two million people upon launch in 2029.

Furthermore, Saudi Arabia has commissioned the world’s largest battery energy storage system (BESS). With a capacity of 7.8 GWh across three sites in Najran, Khamis Mushait, and Madaya, the facility is designed to meet the annual electricity needs of 400,000 households.

HOUSING

Saudi Arabia is intensifying efforts to expand social housing access as part of Vision 2030, with the Sakani programme aiming to deliver two million homes by 2030 while lifting the national homeownership rate to 70 per cent amid rapid urbanisation and population growth. This push addresses affordability challenges in a market strained by rising demand, complementing flagship private developments with targeted workforce accommodation. PIF-backed entities like ROSHN Group and Smart Accommodation for Residential Complexes Company (sarcc) are at the forefront, driving integrated communities and large-scale staff housing to support economic diversification and resident welfare.

Construction work is under way on the infrastructure at ROSHN’s Manar Community in Makkah.

ROSHN Group, the PIF-backed national developer, has signed multi-million-dollar contracts for the development of key land parcels within its flagship Sedra community. Spanning 20 million sq m, Sedra is one of the capital’s largest integrated residential developments. ROSHN is also pushing ahead with its plans of the development of its Alarous community, in Jeddah. The community also benefits from its proximity to the upcoming 11.4-km Marafy canal, a major mixed-use waterfront project set to enhance connectivity and urban appeal. Construction is also under way on the infrastructure works at its Manar Community in Makkah, which has reached 60 per cent overall completion.

Complementing mainstream housing delivery, sarcc is advancing purpose-built staff housing in North Riyadh. The company has signed two non-binding agreements worth SAR2.2 billion to develop large-scale accommodation complexes. With a combined built-up area of 201,000 sq m and 16,000-bed capacity, the projects are designed to address rising demand for workforce housing, with Phase One operations expected to commence in Q1 2029.

REAL ESTATE

According to Mordor Intelligence, Saudi Arabia’s residential real estate market is projected to reach $164.85 billion in 2026, up from $154.61 billion in 2025, and is expected to grow to $227.12 billion by 2031, reflecting a CAGR of 6.62 per cent over the 2026–2031 period. Growth is being driven by sustained government investment under Vision 2030, strong population expansion, and increasing mortgage liquidity, which continue to widen demand–supply gaps and support new project deliveries. Real Estate

Meanwhile, according to Knight Frank’s Destination Saudi 2026 report, up to $6.3 billion in private global capital stands ready to flow into Saudi Arabia’s real estate market following the kingdom’s January 22 opening of property ownership to non-resident foreigners, once regional geopolitical tensions subside. The consultancy highlighted $1.5 billion targeting residential purchases and $3.4 billion for branded residences.

The opening up of the real estate market has resulted in a surge in real estate projects across the country, while other developers are fast-tracking and launching subsequent phases of their projects.

Riyadh is seeing a surge in integrated communities and infrastructure. The $880 million Noor Khuzam project introduces over 3,000 smart residential units near King Khalid International Airport, while Dar Al Arkan is fast-tracking the Shams Ar Riyadh masterplan for completion by late 2026.

The luxury sector is being redefined in Jeddah through high-profile international partnerships. Dar Global has launched the $1-billion Trump Plaza Jeddah and awarded the main contract for the 47-storey Trump Tower Jeddah.

Makkah remains a focal point for transformative urban development centered on the pilgrim experience, with projects such as Masar Destination making significant progress. Among other new project, the King Salman Gate project will introduce 12 million sq m of mixed-use space while the Dyar Al Haram development is offering 4,000 ready-to-own units, marking the largest residential offering for the global Muslim community in such close proximity to the Grand Mosque.

In the Eastern Province, the $26-billion New Dammam, a seaside residential city spanning 32 million sq m, is being developed by Adel Real Estate and Alinma to feature over 15,000 housing plots, waterfront palaces, and an extensive canal system designed to house 180,000 residents.

Also in the Eastern Province, Al Othaim Park is nearing completion. This major mixed-use development by Al Othaim Holding, spanning over 224,000 sq m in Dammam, features retail, residential towers, hospitality, cinemas, and family-oriented spaces